Delivery 2030: A blueprint to transform the UK pension system, deliver the future of retirement and leave no saver behind

Delivery 2030: A blueprint to transform the UK pension system, deliver the future of retirement and leave no saver behind

“The UK is navigating the biggest shift in demographics for many generations, which poses a great threat to the retirement savings system. Today’s savers have no role models, and the system works against them in many ways. On top of that, the recent policy priorities do not address the most fundamental issue – people aren’t saving enough. Now is the time to act and use the time between today and 2030 to implement a plan which will ensure that no saver is left behind.”

– Jamie Fiveash, CEO, Smart UK

Report updated in February 2025

In response to ongoing policy changes, including Mansion House initiatives and the postponement of the long-awaited Pensions Review, this report was reviewed and updated.

Executive summary

Ten years ago, the UK took a radical step in helping savers. It’s time for more action.

Populations are ageing at a time when cost of living crises, climate events, conflicts and financial market fluctuations have exposed fragility in our economic and social systems. Amid this, for many UK workers, the most fundamental question – ‘Will I have enough money to be able to live comfortably in retirement?’ – remains unanswered.

The UK took an unprecedented step towards solving this issue a decade ago, bringing millions of people into pension saving ‘by default’, for the first time through auto enrolment. But it was a single step on a path we must move further forwards on with similar boldness to ensure we avoid huge potential issues facing future pensioners’ finances.

In July 2024 as part of the King’s speech, the Government announced a ‘landmark’ pensions review. The review aimed to ‘boost growth and make every part of Britain better off’.It started with Phase 1 towards the end of 2024, with a focus on productive investment, with Phase 2 originally earmarked for late 2024, aiming to take a much needed look at retirement outcomes and adequacy. However, in December, The Chancellor, Rachel Reeves announced the second phase of the pensions review will be put on hold. Arguably, the most important part of the review, with a focus on improving retirement outcomes and ensuring pension adequacy, has been put on the back burner, prolonging the uncertain outlook currently facing future retirees.

The review was undoubtedly a welcome and overdue deep-dive into the UK pensions system, with industry hopes pinned on it speeding up the delivery of urgent and necessary proposals. Its announcement and subsequent pause have further delayed changes that already had broad consensus. Many of these, such as expanding auto-enrolment and increasing minimum contributions, are referenced in this report. The government must urgently prioritise the second phase of the review in 2025, with these delays only amplifying the ticking of the UK’s pensions timebomb.

Although we were encouraged to see that pension saving has been on the new government’s agenda, we are disappointed that investment into the UK has been the priority. With the retirement savings gap set to have one of the biggest impacts on people’s quality of life for generations, we believe the priority should lie in saver outcomes and ensuring we have a fit-for-purpose DC system to achieve pension adequacy for UK savers now and in the future. To not prioritise this would be to fail UK workers.

As we head towards 2030, we have the opportunity to put everyone in the UK in a better position, ensuring that ‘no worker is left behind’, and that we make the most of the opportunity to build UK pools of capital to support the wider economy, and that we shape a system that provides a better future for all. Now is not the time to lose momentum.

It is encouraging to see a consensus emerging within the industry around some key measures. It is crucial to use the time between now and 2030 wisely and with a strategic focus. However, there has been little clarity on a timetable or a pragmatic pathway for achieving this in the coming years.

Now is the time for the pension industry and the government to work together to create a plan and a timetable to address this.

This paper presents a blueprint for the evolution of retirement saving in the UK. It sets out a series of recommendations with timings for implementation. We are calling on governments to use the time between today and 2030 wisely to put every worker in the UK in a better position for their retirement and ensure that ‘no saver is left behind’.

Our recommendations include:

The delivery of urgent ‘no regrets’ changes, to be scheduled immediately, to radically improve the retirement system and savings of every saver in the UK

A real and urgent focus on the delivery of proposals already in motion but not timetabled: phase in the removal of the lower earnings limit as a threshold to pensionable earnings under auto enrolment, change the qualifying age for auto enrolment from 22 to 18 so that all employees of age 18 and over save automatically, implement the Value for Money (VfM) framework, commit to the timetable for an increased minimum contribution rate and implement the pension dashboard.

Establishment of a new and independent Pensions and Savings Commission to create a truly long-term approach to UK retirement saving

Pensions are long-term savings vehicles and should be governed by long-term thinking. However, much-needed reform has been hampered by short-termism from policymakers. We need to develop a resilient, long-term strategy that transcends the short-term horizons of electoral politics. The commission would bring together representatives of all parts of the industry and government to develop a National Pensions and Savings Strategy for the UK, with cross-party political input and decision-making, providing a long-term roadmap for the next 15-20 years. The chief objective of the new commission’s strategy should be to create a future in which everyone can enjoy a comfortable retirement.

Mansion House 2024

In the Mansion House speech in November 2024, the government outlined their intentions for pensions and investment reform within the DC sector, with aims to consolidate schemes to a minimum size. The push for growth and consolidation seems beneficial for UK pension savers aiming to improve financial outcomes through greater efficiency. However, the real goal is to boost the UK economy, as larger schemes are more likely to invest in UK private markets without requiring contentious mandates. The unfortunate reality is there’s no evidence that the proposed path will achieve either of these outcomes.

The industry agrees: scale alone does not equate to a successful pensions market. Insights from January's consultation with regulators, pension providers, and industry bodies will be crucial in designing a consolidation process that truly serves UK savers' best interests. It is also essential to ensure that competition and innovation continue to play a vital role in the pensions industry. Implementing a system that prioritises transparency, disclosure, and accountability, like the ‘comply or explain’ model would be a more effective way to meet the government’s investment goals. It would also avoid some of the significant challenges raised by consultation respondents.Most importantly, whilst prioritising the initiatives that suit the current Government’s growth agenda, it seems the Government has lost sight of the other policy changes needed to ensure UK citizens are saving enough to live on when they retire. This report aims to highlight these critical challenges, providing a step-by-step approach to tackle one of the most significant problems facing our society today: the future of retirement.

Policy implementation tracker

The tracker shows the current status of proposed changes in February 2025. We argue these would positively impact savings rates and saver outcomes, improving the UK pension system.

1.0 Unlocking barriers: how to fix the system today to protect the future of retirement

The issues facing the retirement system are numerous, well-documented and acknowledged within both the industry and the political sphere (see The context). They are complex, overlapping and interdependent.

Despite these issues, the positive news is that we can make real changes today to protect tomorrow’s retirees. However, this requires boldness, a change in focus, and a will to commit to changes now rather than leaving these to a future set of decision makers.

- If we are bold.

- If we switch the focus of today’s initiatives to ensure they clearly target savers’ needs.

- If we carry this out systematically, with a clear timeline that businesses can understand and plan for.

- If we use this as an opportunity to educate savers at each milestone.

We can make a real difference to the next generation of British retirees and many generations beyond.

July’s general election saw the Labour party sweep to power with a landslide victory. We are calling on the new administration to use the time between 2024 and 2030 to put workers in the UK in a better position for their retirement, with this very bold programme of change, ensuring that ‘no saver is left behind’.

1.1 The solution: seven key elements to include in any plan to adequately solve today’s issues

The current approach to improving the pension system and retirement saving has been piecemeal and it allows individual initiatives to be pushed forward (see The context). However, it does so to the detriment of the ‘key’ stakeholders – workers (of all ages) and employers.

A switch to a more ‘customer-centric’ approach is essential, and to adequately solve the issues highlighted (The context), we believe the following seven attributes are key to successful delivery:

A single strategy

We need to be more strategic and forward-looking. There are lots of ideas, some in conflict with others and with overlapping timescales. This strategy needs to be treated like the broad change programme that it is, and to be comprehensively planned out.

A specific timetable

The current lack of a timetable means years slip by without any progression. This means that important issues continue to be overlooked, including the increase in savings rates which is vital for most workers.

Sequencing

There is a fairly obvious order in which to implement some of the changes, with some being natural precedents or building blocks for others.

Forward-looking enough to provide medium-term certainty

Providing greater certainty to employers and savers about upcoming changes (and the timing of those changes) will create more predictability in employment costs and employee net earnings, allowing all parties to plan better.

Wider support

We must seek input and support from important stakeholders who sit outside the pension industry. The issues we are attempting to tackle are so interlinked with other aspects of people’s social and financial lives that they are impossible to solve through pension-related interventions alone.

Bridging the gap

Changes need to be designed and implemented thoughtfully, and in a way that reduces the need for people to include external influences in decision-making. For example, we should ensure that positive pension-related decisions are ‘no-brainers’ and that we use defaults as much as possible to drive savers towards positive outcomes, without them needing to make complex decisions.

Get people to save enough, but not too much

While we should challenge workers (and their employers) to save enough to target an adequate income for retirement, the approach should be structured in a way that avoids placing too great a burden on those whose money would be better spent elsewhere. For example, saving towards a house purchase, so that they avoid having to pay rent during retirement, would be a more sensible option for some savers.

1.2 2030: pensions nirvana

By the time we reach 2030, we want clear progress to already be in place. Today, huge issues are up in the air. Many of these need to be resolved with urgency, and others clearly placed on a roadmap stretching further forwards.

By 2030, every saver in the UK should be:

Saving for retirement from the age of 18, regardless of income

Saving at a rate at least consistent with the Living Pension

Easily comparing pension fees and investment performance

Viewing all their retirement savings in one place, online, against an adequacy benchmark

Able to make key decisions without the need for complex advice or guidance

In particular, we would like to see:

Clearly defined objective

The objective of the DC pension system clearly defined. In Australia, this was legislated through The Superannuation (Objective) Bill 2023. A similarly clear, shared vision would provide real focus.

Removal of discrimination

Removal of unintended forms of discrimination against women and minority groups in the pension system, for example through elements such as auto enrolment thresholds.

Contributions to achieve adequate savings

Pension contributions beyond Living Pension rates, with minimal increases to employee rates and a clear plan to change contributions further, as required, to achieve adequate savings rates for all.

Automated savings for more workers

Automated pension saving expanded to a greater universe of workers, including younger and self-employed workers.

Trust in (MaPS) pensions dashboard

The Money and Pensions Service (MaPS) pensions dashboard to be recognised as a trusted source with high saver usage levels and expanding functionality, including the ability for savers to easily understand the ‘adequacy’ of their retirement savings.

Automatic tax relief

A pension system which automatically provides savers with the tax relief due to them and continues to incentivise long-term savers – providing clarity and understanding of future changes, for example, threshold changes.

Equal footing for self-employed

Self-employed savers to be on a more equal footing with employed savers, potentially through greater tax incentives, and some form of automatic enrolment.

Higher quality pension schemes

A smaller number of high quality pension schemes which achieve higher returns by investing in more sophisticated assets (aspiring for high value, not low cost), and which take advantage of their scale and technology to achieve lower-cost administration and greater efficiency – passing on benefits to savers in the form of higher growth.

Simplification

A reduction in the need for advice, through simplification and defaulting savers into semi-personalised pathways through and into retirement.

Accessible advice

Accessible advice and guidance beyond the existing MaPS provision – significantly reducing the advice gap.

2.0 Urgent changes: how we can achieve pensions nirvana

The existing piecemeal approach to pension policy – driven by rotating government ministers, differing objectives, a limited set of external voices influencing key decision-makers, and the need to focus on the most pressing matters of the day – has resulted in a lack of deep consideration of the policy changes required to create a better pension system for the future. In turn, this has created confusion (among many stakeholders, but most importantly savers and prospective savers), complexity, unanticipated wider impacts and limited progress towards adequacy. It’s vital that pension policy formation is approached differently to how it has been in the recent past (see The context).

Recent attempts to address systemic issues can be broadly grouped into three themes:

Understanding

Increasing savers’ understanding of the value of their retirement savings.

Quantity

Increasing the amount being saved.

Quality

Making savings work harder, creating more retirement income from the same level of savings.

We present a blueprint plan for the evolution of retirement saving in the UK, setting out below two main recommendations and timings for implementation. We are calling on the next government to use the time between today and 2030 to put everyone in the UK in a better position for their retirement, ensuring that 'no saver is left behind' – shaping a system that provides a better future for all.

2.1 Urgent ‘no regrets’ changes

Reaching a pension nirvana will take some time to achieve. However, that does not mean that progress needs to wait. There are a number of ‘no regrets’ decisions which should be acted upon swiftly, in order to set a timetable for achieving impactful change quickly. The pause on the pensions review has created a policy hiatus, delaying crucial changes. Many of these reforms have been close to legislation for some time but are now on hold. We don’t believe this is the right approach.

Every year in which we fail to act is another step towards poverty in retirement for many.

We should plan and implement these ‘no regrets’ changes in the short term:

Implement the changes set out by the 2023 Private Members’ Bill

– expansion of auto enrolment, targeting completion of these changes by 2028

- Phase in the removal of the lower earnings limit as a threshold to pensionable earnings under auto enrolment, decreasing in two to three stages until it reaches zero so that contributions are being paid from the first pound of earnings. If unchanged, this will negatively affect many in the future, and in particular discriminates against women.

- Change the qualifying age for auto enrolment from 22 to 18, so that all employees aged 18 and over save automatically.

Implement the VfM framework

taking care to avoid unintended consequences such as negatively impacting the likelihood of trustees refraining from certain asset classes.

Set a timetable

for contribution rates to increase, initially targeting 12%.

Implement the MaPS pensions dashboard

with steps made towards including pensions in payment and easy comparison of pension savings against an adequacy benchmark, such as the Pensions and Lifetime Savings Association (PLSA)’s Retirement Living Standards.

Whilst making the changes to extend auto enrolment, it would make sense to consider simplifying some of the auto enrolment requirements to remove complexity through changes to, or removal of specifics like opting out, postponement, re-enrolment, exemptions and exceptions.

3.1 A new pension commission

Creating a true long-term approach, matching the long-term needs of every saver

Bedding-in a number of key changes quickly would not only provide some certainty of near-term changes but also give space and time to focus on the thornier issues that need more consideration and debate. We propose that in order to tackle this deeply and widely enough, an independent Pensions and Savings Commission is created with the objective of implementing a National Pensions and Savings Strategy, with cross-party political input and decision-making.

This commission should provide a long-term roadmap, not just for the next five to ten years but the next 15-20.

Consideration should also be given to whether this becomes a standing commission which has longevity beyond its initial term and objectives. The success of the Pension Commission chaired by Adair Turner (2002-6)1 still lives on, but progress towards the adequacy of savings rates outside the recommendations made by this commission (and, in places, even where recommendations were made) has been limited. The commission’s initial analysis, published in 2004, found that 60% of those aged over 35 were on track to receive an inadequate pension. Depressingly, despite all of the resulting changes made in the years since the commission, this percentage may not have decreased much (accepting that the scale of the inadequacy will probably have reduced). It’s also interesting to note that the Turner-led Pension Commission recommended that a successor body be formed to present follow-up reports every three or four years.2 This did not happen.

3.2 Implementing an effective commission

In order to create an effective commission – as with any major programme of work – it’s important to establish the objectives of the programme and the intended outcomes.

Proposed objectives

The chief concern of a new commission should be how we can create a future in which everyone can enjoy a comfortable retirement.

We know from our annual Future of Global Retirement surveys3, which have polled thousands of UK citizens, that among the top worries for retirement are:

- healthcare costs

- day-to-day living costs

- accommodation costs

- living a limited lifestyle

The implications here related to adult social care in the future are obvious. Taking serious action would allow us to radically change the shape of the UK’s future finances in this respect alone.

We would like to see the Pensions and Savings Commission tackle how we can achieve economic wellbeing and comfortable living in retirement.

Proposed remit

Amongst the topics considered by the commission should be a review of what currently works well within the existing system and what does not, before moving on to consider pension and savings holistically, including topics such as:

Coverage and proposed levels of pension provision, including:

- Private sector, public sector and the State Pension.

- Auto enrolment for self-employed population.

- Viability of continued Defined Benefit arrangements in the public sector, the role of Collective Defined Contribution (CDC) schemes in the public sector and whether any future savings could enhance DC provision for all.

- Consideration of refunds to members who permanently leave the UK, as non-UK national and resident deferred members are estimated to account for over 20% of all deferred DC pension pots.

Levels of saving, including:

- Whether pension saving rates post the ‘no regrets’ changes are still broadly inadequate and need further revision.

- Self-employed pension contributions.

- Potential compulsion of retirement savings.

- How to construct minimum contributions that target adequacy in retirement income without disadvantaging or creating financial challenges for lower earners.

Inequalities in the pension system:

- This covers a multitude of areas but should also cover unintentional discrimination in the current system, for example auto enrolment thresholds which, at present, mean women are twice as likely4 to fall below the threshold.

- Equally, the effect of maternity and subsequent career breaks, with later reduced earnings levels should be addressed to minimise discrimination effects.

Solving the small pots challenge:

- Evaluate the scale of the small pots issue post implementation of the ‘no regrets’ changes, taking into account the size of increased contribution flows

- Consider whether the issue has become predominantly historic and whether something akin to a one-time consolidation exercise would sufficiently remove or reduce the problem

Decumulation structure:

- Understand and articulate the needs of members in decumulation.

- Seek to understand whether the existing product set delivers what members need in decumulation, and partial decumulation.

- Identify any product gaps.

- Consider the nomenclature of the retirement product suite and the role this plays in the misuse of products, including annuities which are poorly understood or valued by consumers.

- The role of CDC in this.

Role of member choice and/or a lifetime provider model:

- Articulate the aims and objectives of both of these models.

- Consider whether a lifetime provider model would deliver sufficient benefit – once the dashboard and other ‘no regrets’ interventions are in place – to justify its creation.

- Whether an alternative model would deliver enough of the desired outcomes.

Taxation, including:

- Whether greater tax incentives would encourage self-employed workers to use the pension system to save for their retirement.

- The complexity of pension taxation and relief, and whether a system could be created under which savers would not need to reclaim tax relief themselves.

- The role of State Pension and the wider benefit system particularly for low-earning savers.

- Whether State Pension provision should be more tailored to a person's broad circumstances, for example, could a reduced State Pension be accessed earlier for those with shorter life expectancy?

- How to continue to support the State Pension system despite the combined forces of an ageing population and a decreasing ratio of workers to pensioners.

- Whether there is a role for a Universal Basic Income (UBI).

Regulation and efficacy of the dual-regulator system

The role of other savings, such as for property/housing, including:

- The interplay between debt, savings, home ownership and retirement.

- How much the pension saving system should also provide an approach by which savers can avoid debt and save for a home, continuing the encouragement of participation in the longterm savings sector whilst helping them meet other financial objectives which might benefit their pension savings in the longer term.

The role of the Pensions Minister

This evolution of retirement saving in the UK calls for change of great scale and pace.

The role of the Pensions Minister is enormously important to the UK’s future, to a level not recognised by its current status. The role has huge implications for all employers in the UK, all workers and their finances, for the immense power of future UK DC pension savings, for future adult social care, and for a just and fair society overall. A Minister of State for Pensions or a Minister of State for a Respectable Retirement, who potentially attends cabinet, would better represent the reality of the position, and provide the seniority required to match its significance in relation to the UK economy and millions of people’s daily lives.

Update February 2025

Emma Reynolds was announced as Pensions Minister in July 2024 by the incoming Labour government. Reynolds proceeded to undertake and announce a number of consultations and objectives, some in partnership with Chancellor Rachel Reeves, but after just six short months in office, Emma Reynolds was replaced by Torsten Bell.

Having had nine Pensions Ministers in the last ten years has resulted in policy inconsistencies, increasing complexity and uncertainty for savers. This has undermined pensions as a savings vehicle and directly hindered progress in pension saving, which will ultimately impact UK savers for generations. Whilst we regard Bell’s appointment positively – given his considerable experience and understanding of pensions and household finances - we are disappointed to have yet another new Pensions Minister.

Bell’s appointment follows the pattern of Reynolds’ before him, in that his role spans both the Department for Work and Pensions (DWP) and His Majesty’s Treasury (HMT). This has the potential to foster a more cohesive approach to pension policy, bridging the gap between the two departments, but runs the risk of initiatives focusing on broader Treasury objectives rather than on delivering best outcomes for pension savers. Bell may be challenged to remain true to this.

Reinstating phase two of the Pensions Review, which focuses on adequacy, along with renewed consideration of the auto-enrolment improvements outlined in this paper, would be a welcome step in the right direction. These changes are urgently needed by the industry and savers to safeguard their retirement.

The context

The state of UK pensions: five crucial issues hampering the future

For years, pension professionals have talked about savers ‘sleepwalking’ into a poor retirement, but industry and employer efforts to raise contribution levels and awareness have failed to create enough change to counter this. In fact, industry experts are increasing their estimates for adequate savings in retirement. In February 2024, the PLSA estimated that a single person will need £31,300 a year for a moderate income in retirement. This represents an increase of £8,000 on its estimate from the previous year, not only owing to rises in food and energy costs but also reflecting savers’ changing expectations about what their retirement looks like. Despite this, auto enrolment contribution rates and thresholds remain unchanged.

Issue 1: The move from DB to DC – a system in flux, with unaddressed disadvantages for savers

While the UK started on the trajectory towards a Defined Contribution (DC) model more than two decades ago, the continuing legacy of the Defined Benefit system means that most current and near-term retirees are not yet fully reliant on DC provision. However, this is changing, and within just a few years we will have a sizeable number of savers retiring with only, or overwhelmingly, DC workplace retirement savings.

This shift across the whole system presents significant disadvantages for savers when compared to a DB system.

- Savers take on all responsibility for ensuring their savings will be sufficient, potentially unknowingly – in a shift of risk from employer to saver.

- It’s often difficult for savers to know whether their savings are ‘adequate’ for their planned retirement.

- Savers are responsible for making key decisions during their savings journey, in the lead-up to retirement and throughout retirement, that will have a profound impact on their retirement income.

Issue 2: Kicking the can down the road: taking action never seems urgent

The backdrop of a pandemic, high inflation, high interest rates and a cost of living crisis has fueled a reticence in some quarters to load extra costs onto people or employers.

However, we risk repeating this mistake indefinitely and never acting because the issues are not considered urgent enough. If a timetable for increasing pension contributions had been agreed several years ago, whilst the exact timings might have been revised to reflect the recent financial challenges, there would still have been progression towards retirement saving adequacy. We continue to perpetuate this.

Issue 3: A lack of strategy and timelines: minimal planned changes to address systemic issues

Currently, the plan to address issues facing today’s workers is limited to:

- Auto enrolment being expanded to apply to workers from age 18, down from the current age of 22)

- A commitment to review the ‘earnings trigger’ and ‘qualifying earnings band’, which would expand the universe of workers captured by auto enrolment regulation and increase the earnings that pension contributions are paid upon.

There is a general acceptance that these changes would be phased in over time, yet the finer details and a timetable for implementation have still not been confirmed. What this leaves us is little in the way of a plan or clear path to improve saving rates in the UK, despite strong support from savers and employers.

In a recent survey of employers, 60% of respondents strongly support the expansion of auto enrolment, underlining a shared commitment to their employees’ futures. They are also keen to see this change take effect quickly, with 26% advocating immediate implementation and 50% keen to see expansion within two years.5

Issue 4: The ‘role model gap’: tomorrow’s retirement does not look like today’s or yesterday’s

The widespread change from DB to DC has meant that there are fewer financial role models for younger generations within their families and communities. Younger generations – but notably, not just the young – who would have typically relied upon parents or grandparents for financial support and guidance, are unable to draw upon their role models’ experiences as directly as previous generations have done. The result is that many workers will be blindsided by the reality of their retirement once they start to understand it better – which, for many, might be at or near the point of retirement.

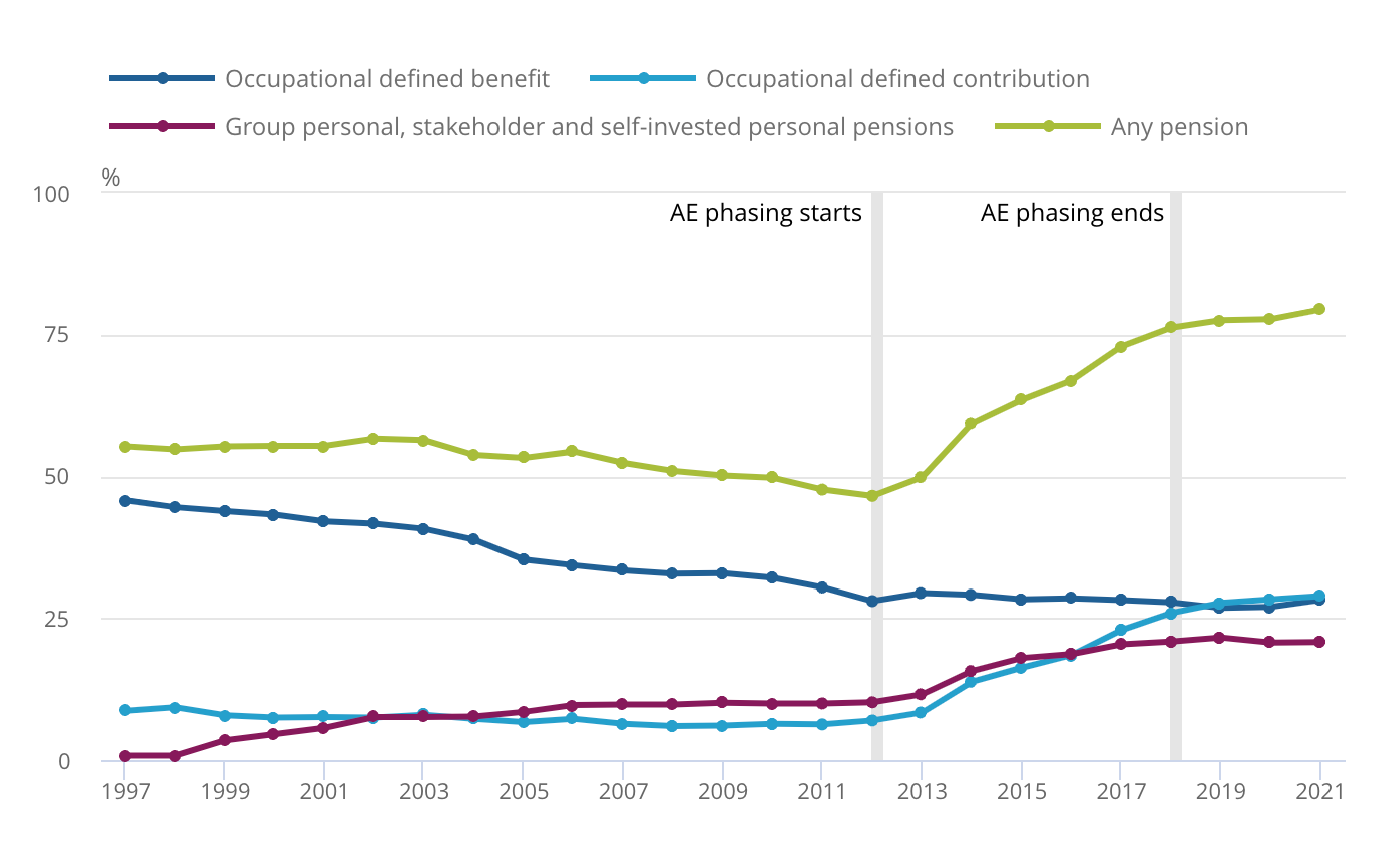

Proportion of employees with workplace pension by type of pension, UK 2001 – 20216

Issue 5: Multiple risks continue to grow: ageing, undersaving, inequality and hardship pose increasing threats to the retirement saving system

Despite the introduction of auto enrolment over ten years ago, current analysis shows a large proportion of the population is still undersaving for retirement, with:

- 38% of working age people, equivalent to 12.5 million, undersaving for retirement

- undersaving increasing to 43% of working age people, equivalent to 14.1 million people, when 75% of a save’s DC pension is converted into an annuity.

There are considerable differences in longevity, health and retirement savings across the UK, with people on lower incomes not living as long as people in more affluent circumstances. The Resolution Foundation reported in December 2023 that income inequality is higher in the UK than in any other large European country.

An outdated pension savings system risks exacerbating these inequalities, perpetuating the retirement ‘haves and have nots’. It also increases the reliance upon state provision. The State Pension is already strained and it is likely to face further challenges as the working population in the UK shrinks and the number of Brits in retirement grows.

It is not clear how longevity will develop in the near term. Prior to the pandemic, we had experienced improvement in mortality rates, yet we now face several health crises (mental health, obesity, NHS provision challenges). Quite how these will turn out is unclear.

Recent attempts at tackling systemic issues

Within the retirement savings industry, and indeed within the political sphere, there is some acknowledgement of the above issues. Recent attempts to address systemic issues can be broadly grouped into three themes:

Understanding

Increasing savers’ understanding of the value of their retirement savings.

Quantity

Increasing the amount being saved.

Quality

Making savings work harder, creating more retirement income from the same level of savings.

Consultations, calls for evidence and other activities around these include:

The missed opportunity: increasing savings

While there is undoubtedly value in each of these initiatives, albeit to vastly differing degrees, none of them addresses what we believe is the biggest issue with DC retirement savings – the significant majority of people are unaware that they are not saving enough.

Whilst each contributes towards the progression of retirement saving in the UK, these initiatives should not be prioritised ahead of changes that will directly impact saving rates. In some cases the suggested changes may be primarily politically motivated and may create a significant distraction, delaying more important and impactful changes from being implemented.

A modern retirement platform, purpose-built for providing workplace pensions

Meet the team

Jamie Fiveash

Chief Executive Officer, Smart UK and Ireland

Jamie is passionate about transforming pensions to make sure that they bring greater value and help improve later life for all people. He was previously Chief Operating Officer at B&CE, where he was instrumental in the design and delivery of The People’s Pension, before joining Smart in 2018. With a background in accountancy and more than 27 years' experience in financial services, Jamie is an experienced and skilful pair of hands to efficiently lead Smart's pension and platform businesses to further significant growth.

Eve Read

Senior Director of Strategic Delivery, Smart UK

Eve is a well-known and respected figure in the retirement savings sector. She spent two decades focused on pensions at employee benefits consultancy Mercer, which included setting up and running the firm’s UK DC consulting business. More recently she worked at the government DC scheme NEST, where she led on business delivery and customer engagement. Eve leads the UK Proposition Team as it builds new features for the Smart Pension Master Trust as well as contributing to the development of Keystone, Smart's global Platform-as-a-Service offering.

Further information

For further information on this report please contact

[email protected] or visit www.smartpension.co.uk.

Disclaimer

This report has been prepared by Smart Pension Limited and/or an entity owned or controlled, directly or indirectly by Smart Pension Limited (“Smart”) solely for information purposes and does not, and is not intended to, create any relationship between Smart and any recipient(s). The report does not create an offer or an invitation to create a contractual relationship with any recipient(s). Nothing in this report should be viewed or construed as advice and Smart is not regulated by the Financial Conduct Authority and the protections of the UK Financial Services Compensation Scheme may not apply. All reasonable efforts have been made to ensure the accuracy of the information in the report, but Smart makes no representations as to the accuracy or completeness of the information and Smart disclaims any liability related to the report. This report is confidential and is not to be shared with any party without the prior written permission of Smart.

Smart Pension Master Trust is authorised and regulated by the UK Pensions Regulator.

136 George Street, London, W1H 5LD

Website: www.smartpension.co.uk

Company registration number: 09026697

1 Pension Commission chaired by Adair Turner (2002-2006)

2 The Turner Report

3 Smart, The Future of Global retirement 2023

4 FT adviser, May 2023

5 Smart Pension, Employer pension landscape 2024

6 Employee workplace pensions in the UK: 2021 provisional and 2020 final results

7 DWP, Analysis of future pension incomes, March 2023

8 Original Pensions Act, 2008